Planned utility-scale capacity additions for 2023 show that solar, wind, and batteries will dominate the United States power sector growth. In the past 10-15 years, renewable energy remarkable growth already resulted in significant reductions of electricity generation from both fossil fuels and nuclear power. As the country pursues the ambitious goal of 100% carbon-free electricity by 2035, renewable energy and batteries are the top priorities, not nuclear power. This is because of greater economic competitiveness and environmental preferences. In line with these empirical observations, the United States Department of Energy projects that more than 80% of the country’s electricity may come from RE in 2035. However, reaching this level of RE penetration will require a strong acceleration of ongoing progress. In this regard, the efficient implementation of the landmark Inflation Reduction Act of 2022 will be decisive.

Solar, Wind, and Batteries to Dominate Growth in 2023

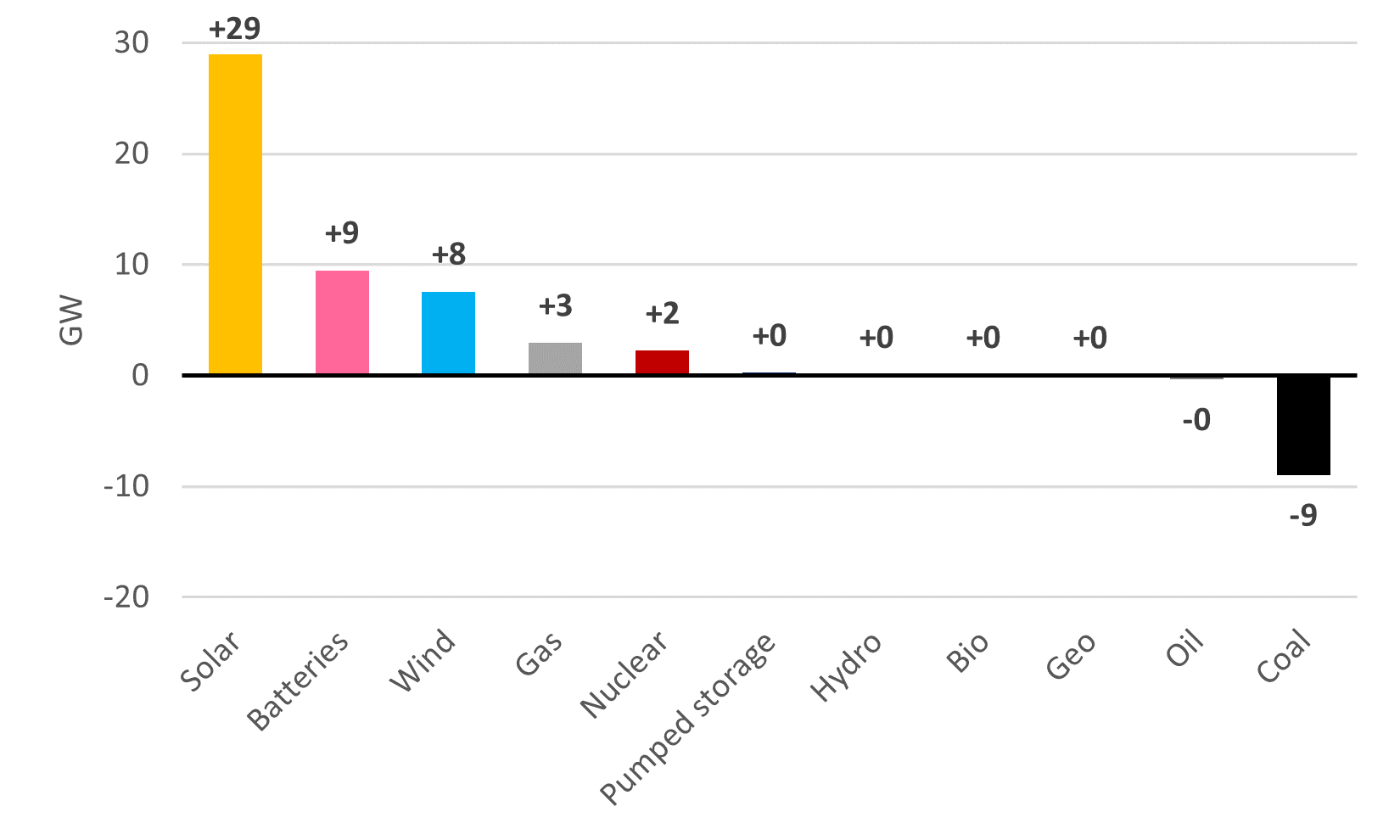

In 2023, according to reporting by the United States Energy Information Administration covering utility-scale power plants exclusively, it is planned that 29 gigawatts (GW) of solar capacity will be added nationwide. Growth in small-scale solar systems may also be expected to be significant. Batteries and wind will compete for the second place with: +9 GW and +8 GW planned, respectively.

It may be emphasized that in 2023 as much batteries capacity is planned to be installed in a single year than the batteries cumulative capacity at the end of 2022. Similarly to solar and wind, the success of batteries comes from economic and technological progresses. Thanks to economies of scale and improved performances, between 2010 and 2022 the price of lithium-ion batteries dramatically decreased from $1,306 per kilowatt-hour (/kWh) to $151/kWh, an 88% reduction.1 The profitability of batteries is based on providing both power grid stability services and trading opportunities.

This year could also see the commissioning of Vogtle-3 & -4, the only two nuclear reactors under construction in the United States. This project suffers from enormous cost overruns (from $14 billion to $34 billion) and a multiyear delay (more than 5 years).

Finally, it is forecasted that coal power capacity will decrease three times faster than gas capacity will increase: -9 GW against +3 GW (Chart 1).

Chart 1: United States Planned Change in Utility-Scale Installed Capacity 2023

Source: United States Energy Information Administration, Electric Power Monthly – Data for December 2022 (February 2023).

Renewable Energy Growth Results in Decreases of Fossil Fuels and Nuclear

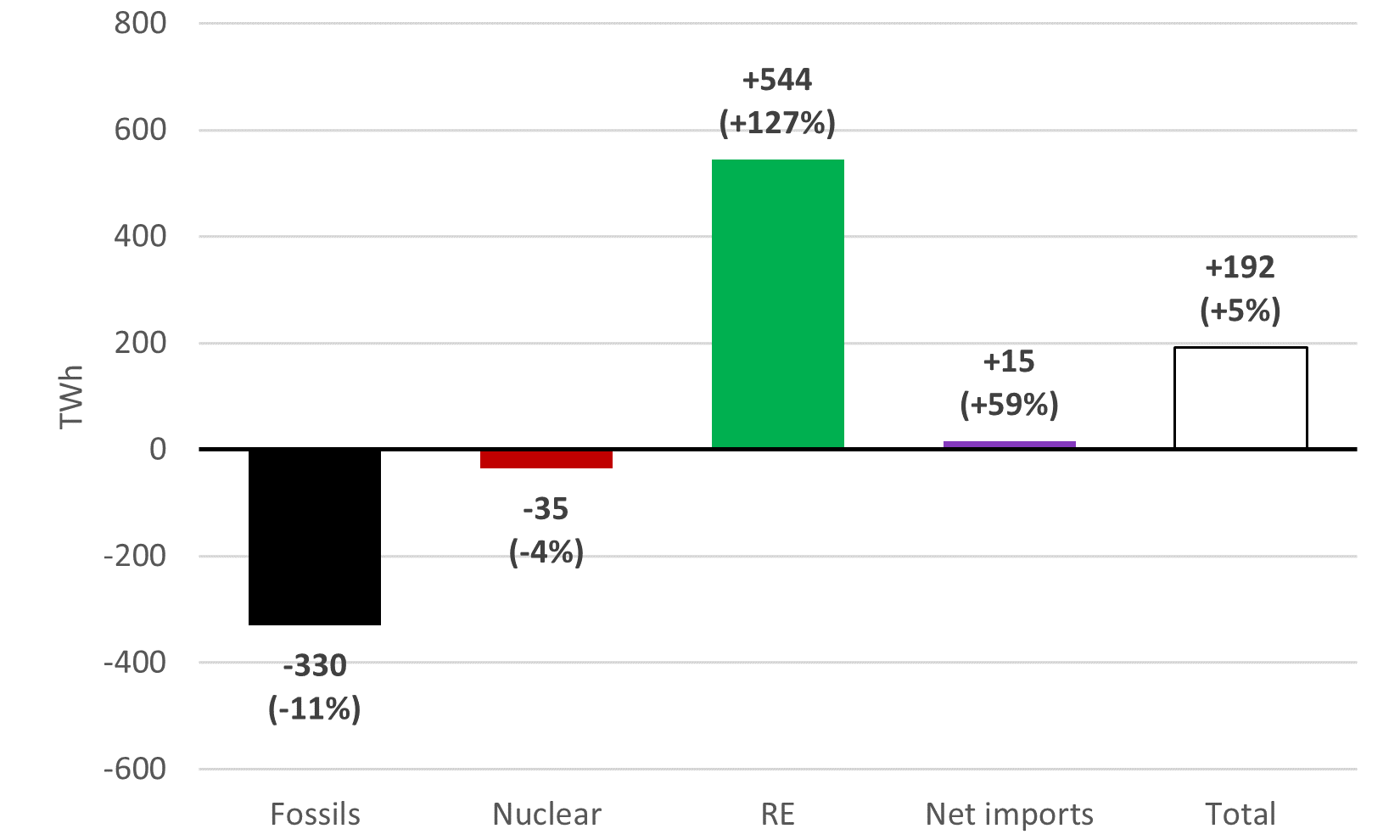

In the United States between 2010 and 2022, renewable energy (RE) grew by a remarkable 544 terawatt-hours (TWh), or +127%. Of this growth, 63% came from wind and 37% from solar. Electricity generation from other RE technologies (i.e., hydro, bioenergy, and geothermal) remained very stable.

This expansion of RE largely exceeded the increase in the country’s total power supply (+192 TWh). This enabled to significantly decrease electricity generation from fossils (i.e., gas, coal, and oil) and nuclear: -330 TWh and -35 TWh, respectively (Chart 2).

Chart 2: United States Change in Power Supply 2022-2010

Sources: United States Energy Information Administration, for 2010; Electric Power Annual 2020 (March 2022), and for 2022; Electric Power Monthly – Data for December 2022 (February 2023).

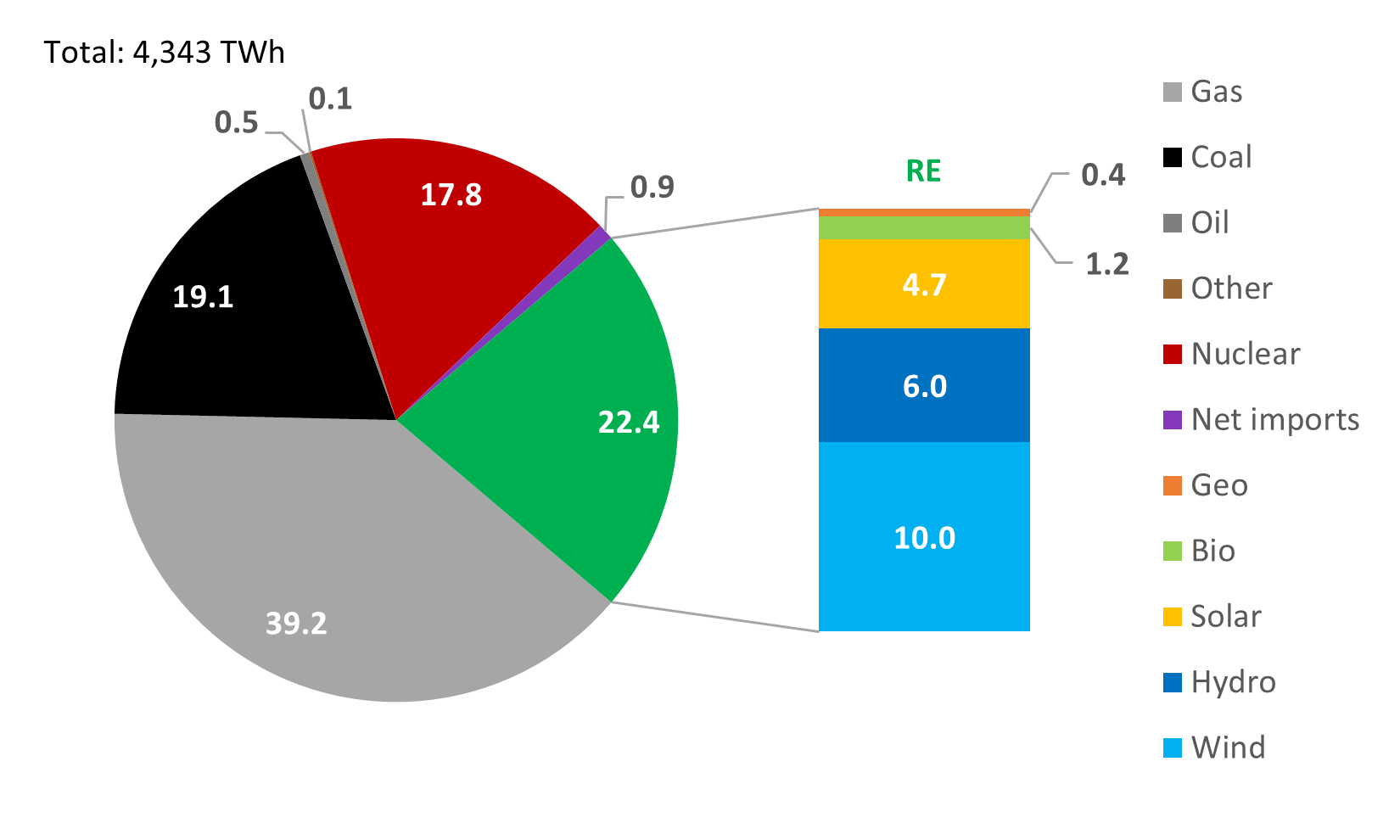

In 2022, the share of RE in the United States power supply reached 22.4%. Compared to 2010 when the share of RE was only 10.3%, this is more than a doubling. For the second time after 2020, in 2022, the share of RE exceeded again both those of coal and nuclear (19.1% and 17.8%, respectively). The next challenge for RE is to close the gap with gas which is the dominating energy source for electricity generation in the country (39.2% of total power supply) (Chart 3).

Chart 3: United States Power Supply Mix 2022

Source: United States Energy Information Administration, Electric Power Monthly – Data for December 2022 (February 2023).

Renewable Energy and Batteries Are Top Priorities for 100% Decarbonization, not Nuclear Power

The United States is now pursuing the ambitious goal of 100% carbon-free electricity by 2035. Towards this goal it is clear that RE and batteries are top priorities, simply because they outcompete nuclear power economically and environmentally.

First, new RE and batteries can be deployed much faster and at significantly lower costs than new nuclear power. For instance, BloombergNEF estimates the levelized cost of electricity of these new technologies in the United States in 2022 2H as follows: $106 per megawatt-hour (/MWh) for non-tracking solar PV + batteries, $72/MWh for onshore wind + batteries, and $351/MWh for nuclear power.2

Second, among decarbonized technologies, RE and batteries are often preferred to nuclear power by electricity consumers. This is because RE and batteries are seen as “clean” technologies whereas nuclear power is only seen as “carbon-free”. This distinction is critical. A lot of consumers reject the radioactive waste produced by the nuclear power industry. This environmental awareness strongly favors RE over nuclear power in the United States. This is important because American businesses are very active to meet their decarbonized electricity needs with RE. In fact, the United States is by far the world leading country for RE corporate procurement. As of early 2023, the United States alone accounted for 61% of the global corporate RE power purchase agreements.3

Moreover, the prospects for the nuclear power industry in the United States are rather gloom.

With the exceptions of Vogtle-3 & -4, no other nuclear reactor is currently under construction in the country. This makes it almost impossible that new reactors can start supplying electricity by 2035, except maybe a few small modular reactors which will not provide meaningful capacity additions.

As for existing nuclear reactors, recent political efforts have focused on subsidies to avoid additional permanent shutdowns due to lack of economic competitiveness. In the United States between 2013 and 2022, 13 reactors (10 GW) were closed.4 In addition, as of July 2022, 18 reactors (18 GW) had been rescued.5 Thus, maintaining electricity generation from nuclear power at its current level is difficult. With the ongoing electrification, replacing fossil fuels in transport and heating & cooling, the share of nuclear power in the United States power supply is likely to fall.

In line with these empirical observations, in 2021, the United States Department of Energy published a report entitled “Solar Futures Study”. This report envisions a deep grid decarbonization by 2035.

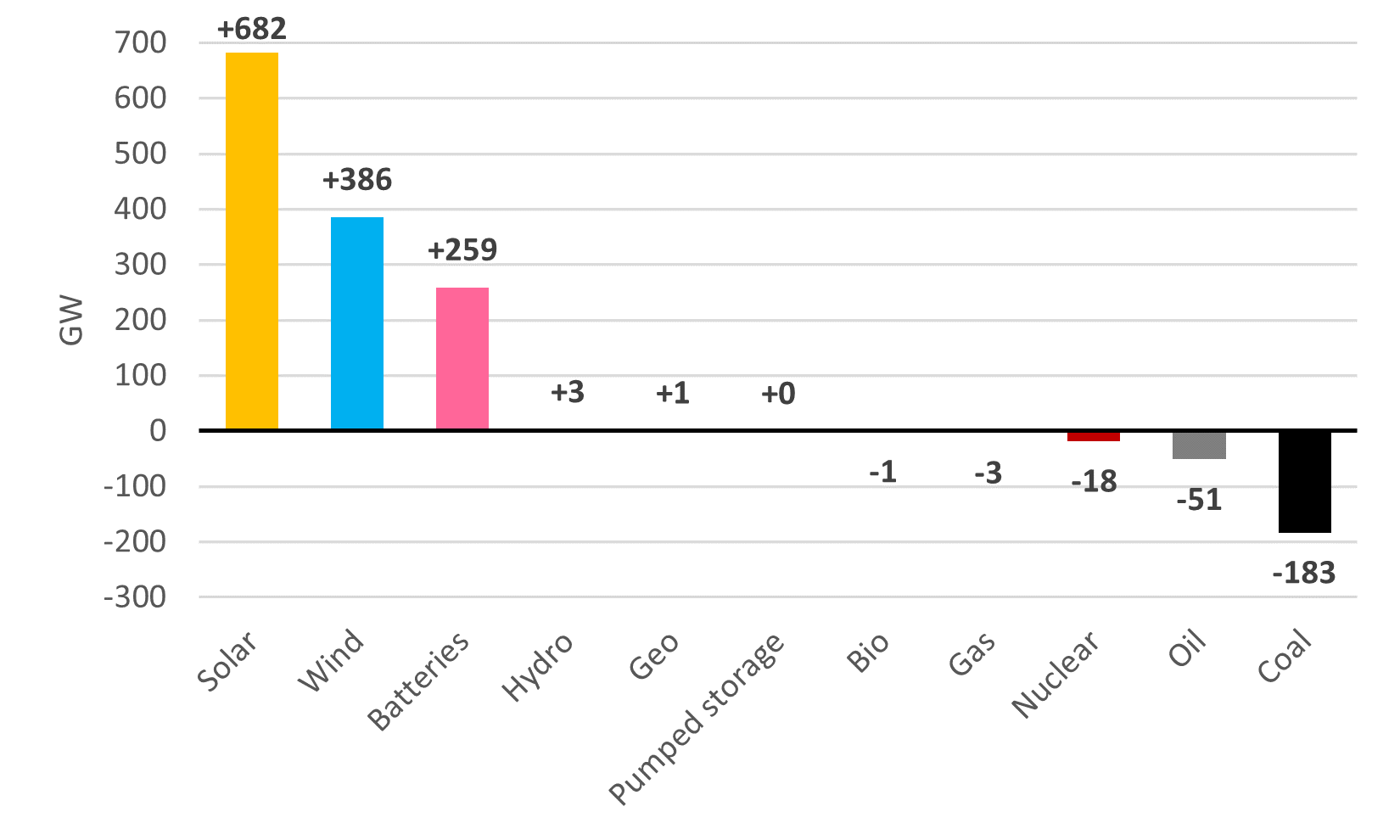

In the decarbonization scenario “Decarb”, it is found that to achieve a 95% reduction in carbon dioxide emissions from 2005 levels by 2035, solar, wind, and batteries are the undisputed three most important technologies to expand between 2020 and 2035: +682 GW, +386 GW, and + 259 GW, respectively. The powerful combination of RE and batteries also ensures stability of power supply to a large extent. This greatly limits the needs for other dispatchable technologies such as fossil and nuclear generators. (Chart 4).

Chart 4: United States Change in Installed Capacity 2035-2020, Projection “Decarb” Scenario

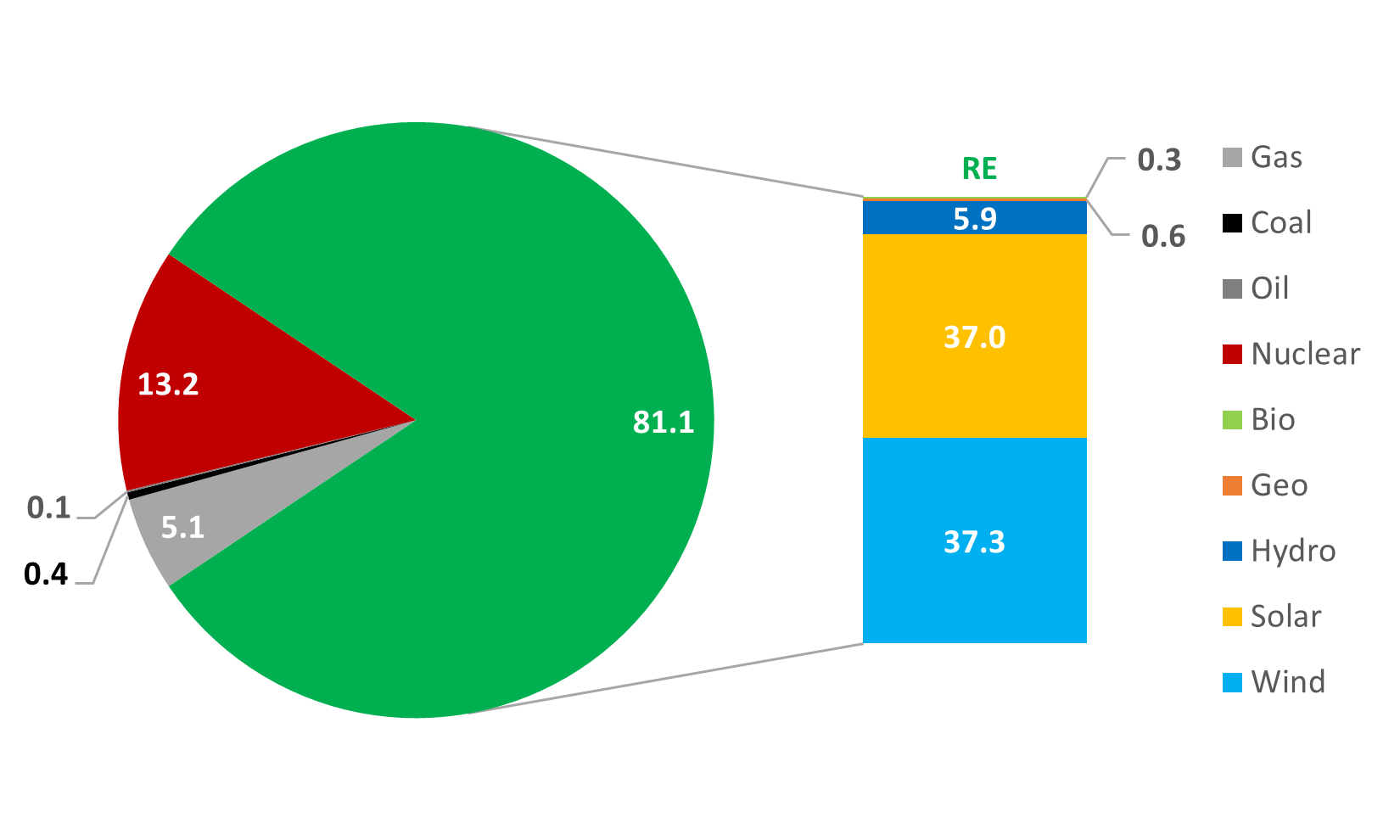

As a result of these transformations, it is projected that RE will strongly increase and account for 81.1% of the United States electricity generation mix in 2035. Together, solar and wind reach almost three-quarters of the country’s electricity generation mix. The share of nuclear power slightly decreases to 13.2%. (Chart 5).

Chart 5: United States Electricity Generation Mix 2035, Projection “Decarb” Scenario

The Role of the Inflation Reduction Act to Accelerate Progress

Fully decarbonizing the United States power sector by 2035 is certainly an ambitious race against time as it means approximately quadrupling the share of RE in the United States power supply in the next thirteen years.

In this regard, the adoption of the Inflation Reduction Act (IRA) in August 2022 is a major progress.

The IRA of 2022 is the single biggest climate & energy investment in the United States history.6 Its triple goal is to bring down energy costs, increase energy security, and reduce greenhouse gas emissions.

The IRA supports energy reliability and cleaner energy production coupled with massive investments in American clean energy manufacturing.

Regarding domestic clean energy manufacturing more specifically, over $60 billion are dedicated across the full supply chain of clean energy and transportation technologies. For examples:

• $30 billion for production tax credits to accelerate manufacturing of solar panels, wind turbines, batteries, and critical minerals procesing.

• $10 billion for investment tax credits to build clean technology manufacturing facilities, like solar panel, wind turbine, and electric vehicle factories.

Furthermore, complementary policies to accelerate the decarbonization of the power sector also include tax credits for decarbonized sources of electricity (including RE and nuclear) and energy storage, and roughly $30 billion in targeted grant and loan programs for states and electric utilities.

The total amount of spending for RE and nuclear under the IRA is not yet determined. However, an early estimate projects the production tax credits for existing nuclear reactors to cost $30 billion.7

With the announcement of these strategic initiatives, the United States has demonstrated that it is ready to accelerate its decarbonization efforts. Efficiently implementing them will now be decisive to meet the country’s 100% carbon-free electricity 2035 goal. This should start by rapidly issuing key regulatory guidance businesses are currently waiting for.

- 1BloombergNEF, Lithium-Ion Battery Price Survey 2022 (December 2022) [subscription required].

- 2BloombergNEF, Levelized Cost of Electricity 2022 2H Update (December 2022) [subscription required].

- 3BloombergNEF, Corporate Power Purchase Agreements – Updated February 15, 2023 (accessed March 13, 2023) [subscription required].

- 4International Atomic Energy Agency, Power Reactor Information System: Country Statistics – United States of America – Updated March 13, 2023 (accessed March 14, 2023).

- 5Mycle Schneider, The World Nuclear Industry Status Report 2022 (October 2022).

- 6Senate Democrats, Summary of the Energy Security and Climate Change Investments in the Inflation Reduction Act of 2022 (undated).

- 7Mycle Schneider, op. cit. note 5.